What a Valuation Multiple Actually Tells You (And What It Doesn’t)

In 2013 I bought a stock because its P/E ratio was 7.

That was the whole thesis. Seven. The market average was around 18. I figured I was getting the same dollar of earnings for less than half price.

I was wrong.

The earnings were about to fall off a cliff. The “7” was the market screaming at me, and I mistook it for a discount. I held for 14 months and sold down 40%. Best tuition I ever paid, but it stung.

Here is what I didn’t understand back then: a valuation multiple is not a price tag. It’s a relationship.

What a multiple actually is

A multiple compares what the market will pay for a company to some financial number that company produces.

Price-to-earnings compares price to profit. Price-to-sales compares price to revenue. EV-to-EBITDA compares the whole enterprise to a rough cash earnings figure.

That’s it. One number divided by another number.

The trap is treating that single number as a verdict. “P/E of 30, expensive.” “P/E of 10, cheap.” I did exactly that for years. It cost me real money.

Let me show you why with a company most people think they understand: Meta.

Meta in 2022

Go back to the fall of 2022.

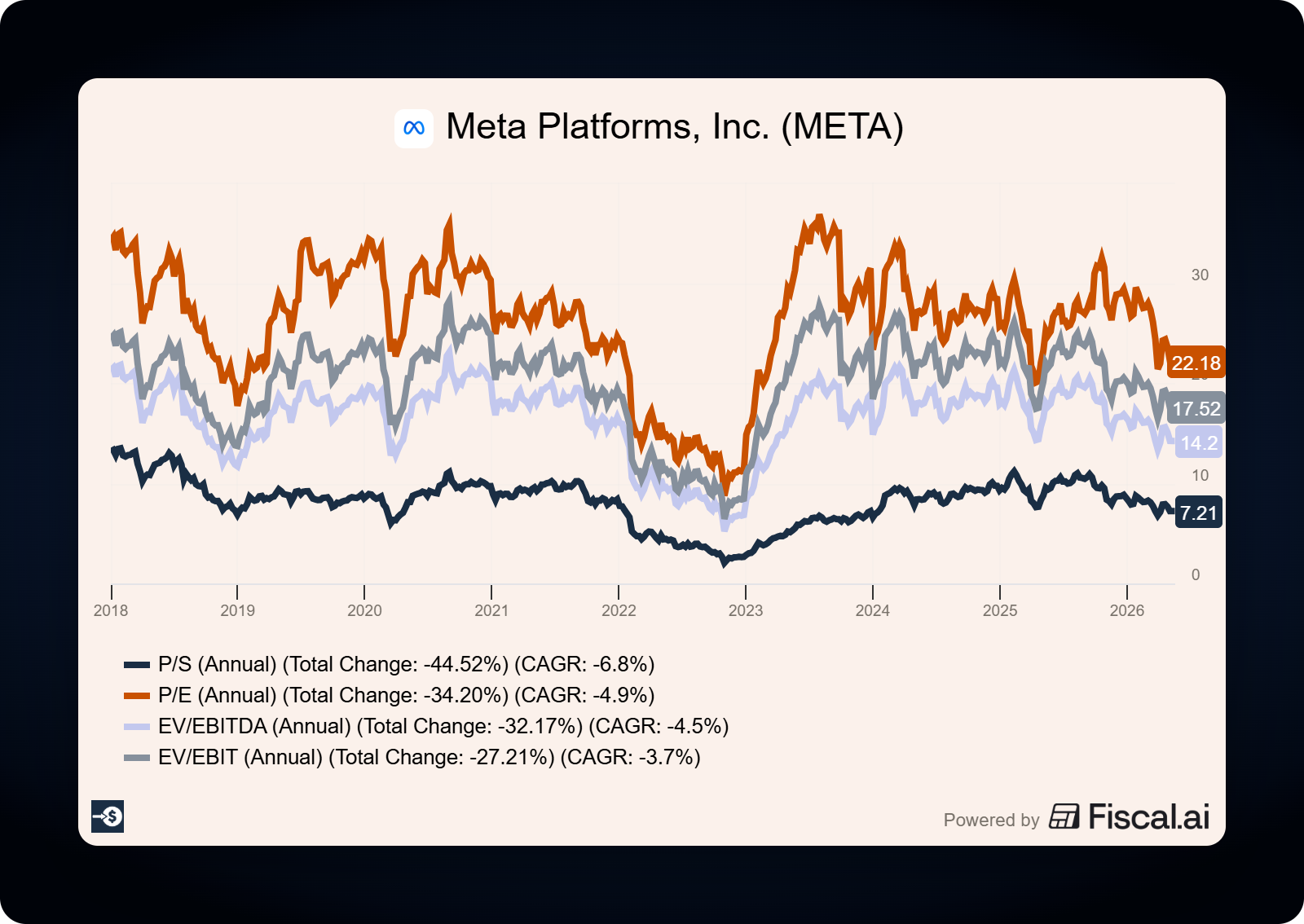

Meta stock had fallen from roughly $380 to around $88. A drop of about 76%. The price-to-earnings ratio compressed into the low teens. By one common measure it touched about 13.

By the simple rule I used in 2013, Meta in November 2022 was screaming cheap. A double digit multiple on a company that prints cash.

Plenty of smart people looked at that low number and saw a bargain. Plenty of other smart people looked at the same low number and saw a melting ice cube. Reality Labs was burning more than $10 billion a year. Apple’s privacy changes had blown a hole in the ad business. Revenue actually shrank in 2022, the first annual decline in the company’s history.

Same multiple. Two completely opposite stories.

The multiple didn’t tell you which story was true. It only told you what the market would pay relative to last year’s earnings. The hard work was figuring out whether those earnings were going up, flat, or down.

They went up. A lot. Meta cut costs, the ad business recovered, and the stock went on to one of the great recoveries in megacap history. But that was a judgment about the business. Not a number you could read off a screen.

If you'd rather understand a P/E than memorize one, this is what the newsletter does every week. One lesson, no hype.

The same trap, in reverse

Now look at Meta in early 2026.

The stock trades somewhere in the $610 to $670 range depending on the day. Trailing earnings per share is roughly $23 to $28 depending on which adjustments you use. That puts the P/E in the low-to-mid 20s.

Meta’s own 10 year average P/E is around 27. So today’s multiple sits a touch below its own history, on a far larger and more profitable business than the one from 2022.

In 2022 a low multiple looked cheap, and the real question was whether earnings would survive. In 2026 a normal looking multiple sits on a company pouring tens of billions into AI infrastructure, with the same question underneath: are these earnings going up, flat, or down?

The number changed. The actual work did not.

Why the same multiple means different things

This is the part the cheat sheet gets right and most investors skip.

A P/E of 22 on a company growing earnings 20% a year is not the same as a P/E of 22 on a company shrinking 5% a year. A P/S of 8 on a software business with 80% gross margins is not the same as a P/S of 8 on a grocery chain earning 25%.

Before a multiple means anything, you have to hold a few things constant. The growth rate. The profitability. The industry. The size. The durability of the earnings.

Those comparability factors aren’t footnotes. They’re the entire ballgame.

A multiple on its own answers one small question: what is the market paying right now relative to a recent financial figure. It does not answer the question you actually care about, which is whether this is a good business at a fair price.

What I do now

I still look at multiples. Every day. They’re fast, they’re everywhere, and they’re great for a first glance.

But I treat a multiple as a question, not an answer.

Low multiple? My first thought is no longer “cheap.” It’s “what does the market think is about to go wrong here, and is the market right?”

High multiple? Not “expensive.” It’s “what growth and durability does this price assume, and is that realistic?”

Meta taught that lesson twice. Once when a low number was a trap for some and a gift for others. Once when an ordinary looking number quietly priced in an enormous bet on AI spending.

The number was never the answer. The number was the start of the question.

Here’s your one action for this week. Pick a stock you own. Find its P/E. Then finish this sentence, out loud or on paper: “This multiple makes sense only if earnings do ____ over the next 5 years.”

If you can’t finish that sentence, you don’t own a valuation. You own a number.

Wishing you investing success, Brian

P.S. If this shifted how you look at a P/E even slightly, that's the entire point of the newsletter. One short lesson, every Saturday, free.