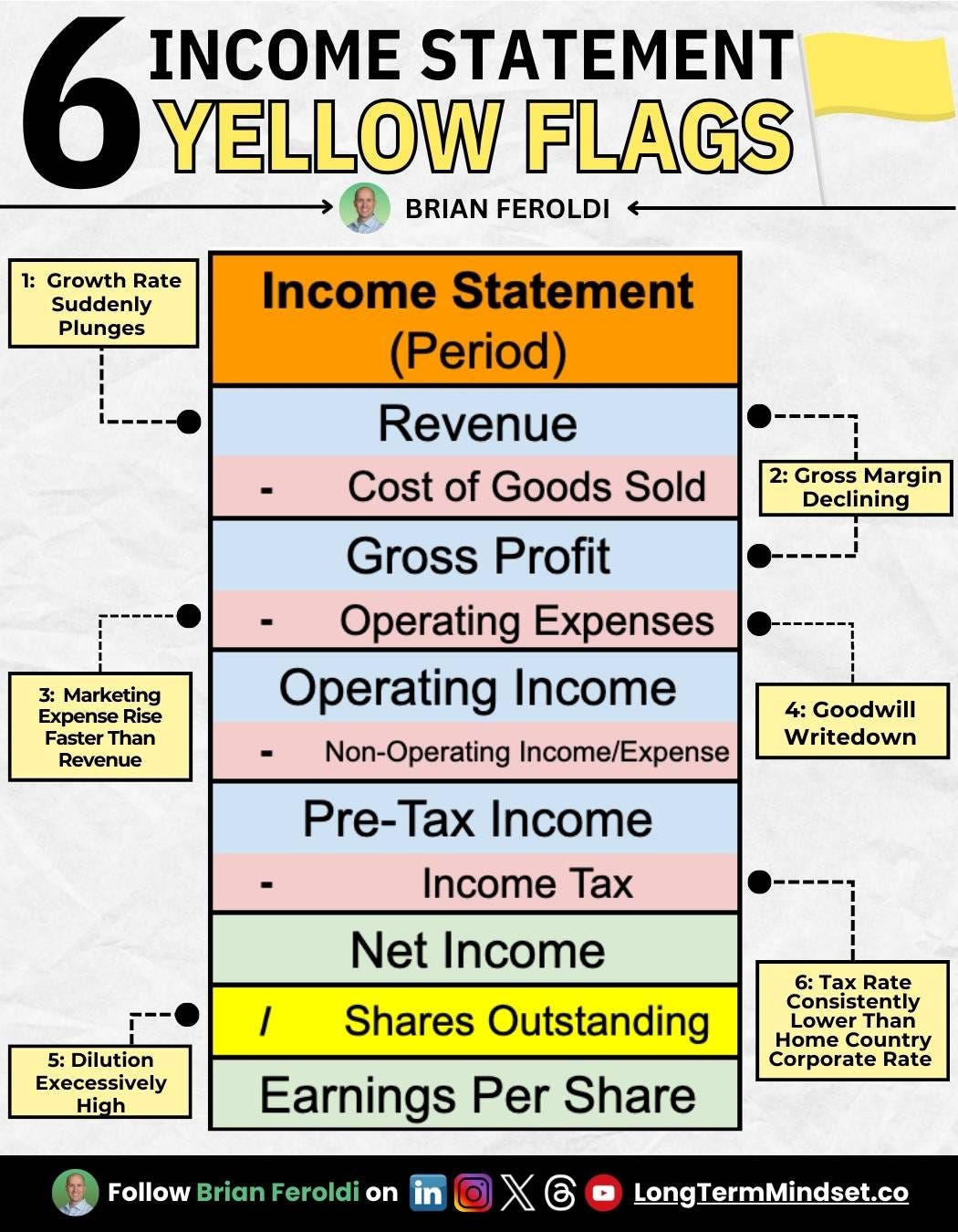

Income statement yellow flags

As we learned in a previous lesson, the income statement shows investors if a company is profitable by giving investors key metrics such as revenue, expenses, and income.

In that same lesson, we defined the income statement’s line items and briefly explained the significance of each.

Today, we will look at six yellow flags you can quickly identify when reviewing a company’s income statement.

1 - Revenue growth declining rapidly

Revenue is the engine that powers everything else in the company. Which direction a company’s top line is moving is extremely important to every other number downstream of revenue on the income statement.

When growth suddenly slows, it’s essential to understand why the company is selling fewer products or booking its services less.

Rule of thumb: Revenue growth will slow as a business matures, but the decline will typically be gradual. When it’s sudden, it usually indicates something is wrong.

2 - Gross margin declining

Gross margin might be the most important metric of a company’s financial performance. It is essentially the money that the company keeps after subtracting out the direct costs associated with producing its goods and/or providing its services.

When gross margin declines, it means a business is keeping less of its sales either because production costs have increased or it is charging less to its customers.

Small changes in gross margin can quickly add up to big changes in earnings, so watch this number carefully!

Rule of thumb: When gross margin declines, it could be a sign that the company does not have pricing power with customers or bargaining power with suppliers.

3 - Sales and marketing rising faster than revenue

Importantly, this refers to sales and marketing as a percentage of revenue, not on an absolute basis.

As a company gets larger, it should the company should be able to spend less on sales and marketing in relation to its overall revenue. If a company must spend more and more to keep attracting customers, that’s not a good sign.

Rule of thumb: Marketing costs should scale with the company as it grows.

4 - Goodwill write-downs

This happens when management recognizes it overpaid for an acquisition, essentially saying it destroyed shareholder value.

The size of the write-down relative to the acquiring company matters a great deal.

In 2015, Microsoft took an impairment charge of $7.6 billion for its Nokia acquisition. That was nearly the total amount it paid to acquire Nokia’s smartphone business! While that’s a huge sum, compared to Microsoft’s approximate $350 billion market cap at the time, it was a relatively minor blunder.

For smaller companies, the write-down could be less in absolute dollar terms but matter much more.

Rule of thumb: Goodwill write-downs are a black eye on a company’s financials and an admission that management destroyed shareholder capital.

5 - Excessive share dilution

Stock-based compensation can be a great way for companies to align employee incentives with the company’s goals without burning cash. This is especially important for young companies that are still growing fast but are not yet profitable.

However, the practice can be easily abused, too. Share dilution hurts shareholders as their stakes represent a lower percentage of company ownership.

So, how can you tell when stock-based compensation crosses the threshold from being a smart practice to excessive?

Rule of thumb: When a company grows revenue quickly (>25%), we’re okay with up to 3% annual dilution. When a company’s revenue growth slows to 10% or less, we want share dilution to be under 1%.

6 - Tax rate consistently lower than its home country’s corporate tax rate

If a company works hard to lower its tax rate, it could reveal a culture that works hard at deception. Be careful because the same company could also be working hard to deceive shareholders.

As with the balance sheet’s yellow flags, these flags signal caution.

Just as when your car’s dashboard flashes a check engine light, it could indicate a minor or a major issue. The driver’s primary takeaway should be that something under the hood requires attention.

In some cases, when a company exhibited one or more of these yellow flags, shareholders were rewarded with outperformance for holding onto their shares as the company worked through its issues.

Accounting is the language of business, but it is filled with nuance. There are very few set rules that require prudent investors to buy or sell immediately.

Instead, these yellow flags on a company’s income statement should signal to the investor that it’s time to look under the hood.

Wishing you investing success,

Brian